EU Hydrogen Bank: 1.3 billion change the distribution

8 min read

On May 7, the EU Hydrogen Bank concluded its third round: €1.3 billion for green hydrogen projects, 58 bids, six times oversubscribed. At the same time, several German states are accelerating solar mandates. For SME suppliers, this shifts the sales playbook overnight.

Key Takeaways

- Demand is real-and so is the funding. The EU Hydrogen Bank auction was six times oversubscribed, plus a separate €12 billion initiative from the Commission’s own resources. German suppliers eyeing this funding corridor must now sharpen their sales focus toward project developers, EPC contractors, and industrial consortia.

- Account-based marketing beats broad reach-by a mile. Our spring 2026 market mapping puts Europe’s key buyers at around 200 project developers and industrial consortia. For a mid-sized sales team of five, account-based marketing isn’t just nice to have-it’s the only method with a realistic hit rate.

- CSR fluff won’t fly. Project developers and EPCs now screen suppliers’ sustainability data as a funding criterion. Greenwashing slides will get you filtered out. Verifiable Scope 1 and Scope 2 emissions data will become a mandatory attachment in bids within the next twelve months.

RelatedCloud Costs: A C-Level Priority / Gartner: $2.52 Trillion AI Spending

How the EU Hydrogen Auction Reshapes the Playing Field

The EU Hydrogen Bank’s third auction round isn’t the first-but it’s the one sending the clearest signal. 58 bids, eleven countries, €1.3 billion in the pot, and a total request volume exceeding €8 billion. For the German government, the timing couldn’t be better: H2Med, the planned hydrogen pipeline from the Iberian Peninsula through France to southern Germany, is now exploring extensions toward Morocco and Mauritania. If these gain traction in the next 24 months, Germany’s industrial strategy will shift noticeably for the first time since the 2009 Desertec wave-moving away from purely domestic power generation.

Here’s what matters for SME suppliers: The funding euros won’t land directly in your accounts. They’ll go to project developers, who will decide on EPC contracts for electrolyzers, storage, and grid connections in the next two quarters. If you want visibility in these tenders as a German supplier, you need to be at the table during the consortium phase-not in a last-minute sprint four weeks before contracts are signed.

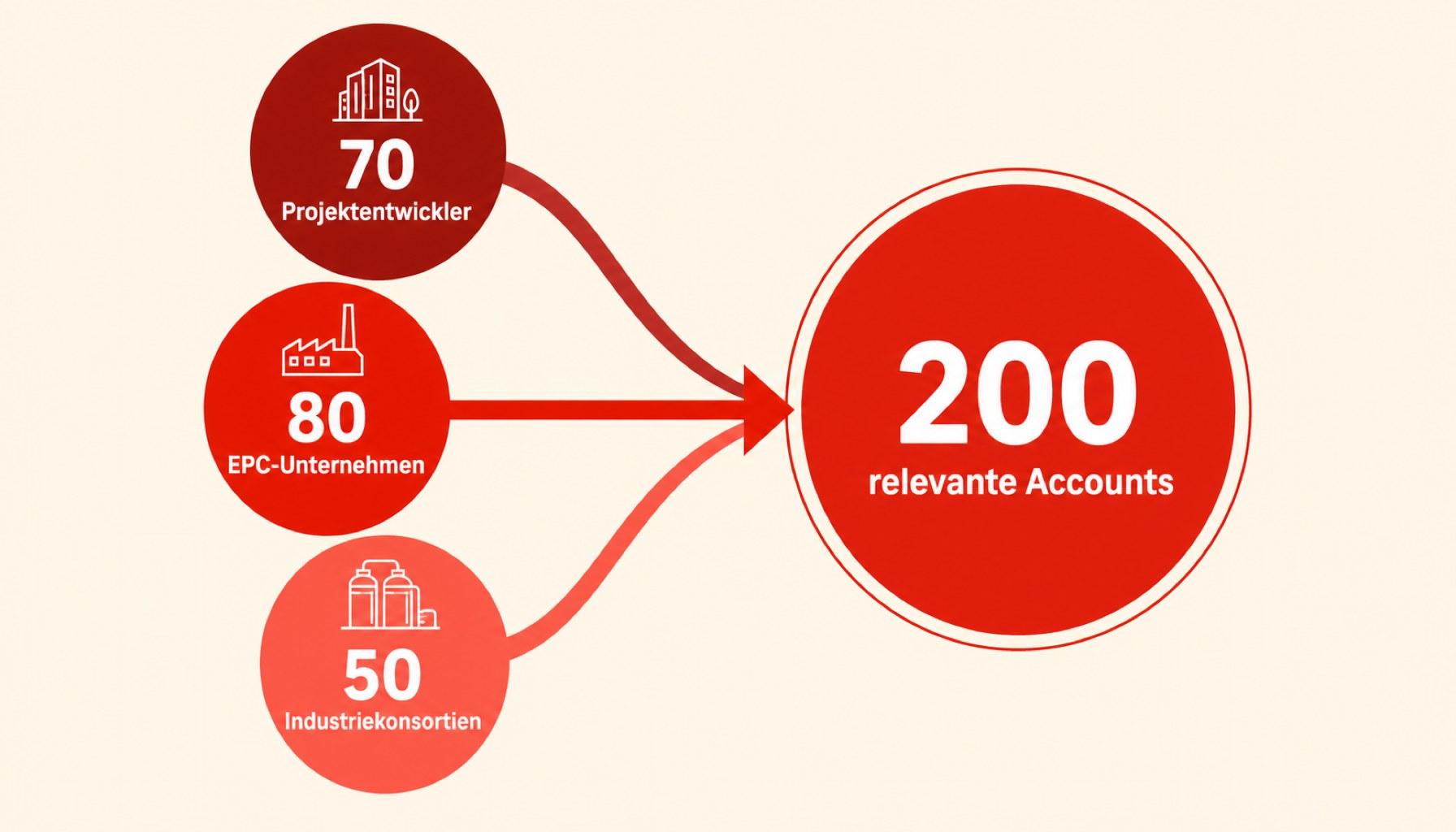

Why Sales Must Shrink to 200 Targets

In spring 2026 we mapped the relevant buyer landscape for an engineering supplier in Europe: roughly 70 major project developers in the solar and hydrogen segments, 80 EPC general contractors tied to the EU hydrogen pipeline, and 50 industry consortia planning large-scale hydrogen purchases within the next 18 months. That totals an estimated 200 account addresses with meaningful hit probability. No more.

For a traditional mid-market marketing pipeline, this is a paradigm shift. 200 accounts means no mass emails, no inbound-funnel games, no reliance on performance campaigns. Instead, it demands an account-based marketing setup that is personalized from day one: one buying center per account with three to five roles, a content track with focused materials, and a sales cycle of nine to fifteen months. If you approach this using the usual B2B logic-where reach is converted into lead quotas-you’ll miss entirely.

Reach is a vanity metric as long as nobody acts on it. In hydrogen pipeline procurement, the only metric that matters is whether you appear on the internal vendor list during the consortium phase. That’s a list entry, not a click-through rate.

What CSR Communication Must Deliver Now

The EU Hydrogen Bank auction and national funding lines now tie funding to sustainability data across the supply chain. This isn’t new, but in 2026 it will be rigorously enforced. Over the past three months, EPC general contractors have begun demanding Scope 1 and Scope 2 data from suppliers as a qualification filter; some tenders now also require Scope 3. Without robust figures, you’re out at the first gate-before your proposal is even read.

Marketing platitudes won’t cut it. “We take responsibility” as a headline in the sustainability report is worthless in an EPC’s procurement filter. What counts are verifiable data on energy sourcing, supply chain, and CO₂ per product. Mid-sized suppliers still lacking this should spend the next nine months not on a new website, but on building the data foundation their sales teams need to present in the buying center.

A real-world example from 2026 sales practice: an inverter manufacturer halved its sales-cycle speed for EPC accounts by standardizing Scope 1 and Scope 2 data per product line in the proposal phase. Not because marketing improved-because the material no longer got stuck in the compliance filter.

Three Concrete Steps for the Next 90 Days

- Sharpen the account list, don’t lengthen it. If your HubSpot or Salesforce currently tracks 1,500 accounts, build a sub-list of no more than 200 for the hydrogen and solar funding corridor. Criteria: ongoing or planned EU auction participation, EPC mandates in DACH or the Iberian Peninsula, industry consortia in the Reboot-Germany funding lines. Anything else is wasted effort.

- Map the buying center by role. Identify three to five roles per account: project lead, procurement manager, ESG lead, technical spec owner. Targeting only the classic buyer misses the pre-qualification phase. Sales cycles for consortium tenders begin during the pre-EPC spec definition, not at the RFP stage.

- Standardize sustainability data per product line. Scope 1 and 2 are mandatory; Scope 3 is coming. Delivering this as a standard attachment in the proposal phase gives measurable lift in the EPC filter. Relying on the sustainability report gets you rejected.

Frequently Asked Questions

Is account-based marketing worth it for a mid-sized company with five salespeople?

In the hydrogen and EPC corridor by 2026, yes; in the classic mass market, usually not. The dividing line is the complexity of the buying center: ABM pays off when three or more roles influence each account and the sales cycle exceeds six months. Both conditions apply in hydrogen tenders. In transactional mid-market business with short cycles, traditional demand generation often remains the more sensible choice.

How quickly should Scope-1 and Scope-2 data be available?

No later than Q4 2026 for the next EU auction round in spring 2027. Those starting now can use 2025 financial-year data with a robust methodology. Those beginning data collection in autumn 2026 will arrive too late.

What role do national funding lines play alongside the EU auction?

A significant one. Germany and Spain have launched parallel funding schemes for hydrogen infrastructure and solar expansion alongside the EU Hydrogen Bank. Sales teams must map consortia against both pools, as many projects stack incentives. Tracking only the EU list misses half the tenders.

Is the Desertec idea back now, or is it still just marketing fluff?

Fundamentally different from 2009. Policy now has a lever, industry has concrete project developers, and pipelines are in permitting. What was missing in 2009 was an affordable scaling mechanism-now provided by the EU Hydrogen Bank. Whether it suffices will be decided in the next 24 months in real EPC projects, not political announcements.

Where should engineering suppliers invest their next Salesforce upgrade?

A clean ABM extension with buying-center mapping, an intent-data feed, and an interface into the ESG data foundation. Buying another demand-gen tool instead will not make you visible in hydrogen pipeline tenders.

Editor’s Reading List

- AI in Accounting: 78 Percent of Mid-Market Transactions Still Hidden

- Cloud Costs Are a C-Suite Issue: When CFOs and CIOs Stop Planning in Silos

- M&Amp;A Rarely Fails on Price: 180 Days Decide the Outcome

Read more on MyBusinessFuture

MyBusinessFutureFujitsu’s AI Platform: Three Implications for SMEsMyBusinessFuturePragmatic Modernization Triumphs Over Metropolitan Master PlanMyBusinessFutureWhoever Reforms in City Hall Must Be Able to LeadMore from the MBF Media Network

cloudmagazinAWS and Nvidia: GPU Million Forces Platform Teams to RethinkDigital ChiefsRaw-Materials Policy Is Now Tech PolicySecurityTodayNIS2 Compliance for Mid-Market Firms: Practical StepsSource for cover image: Pexels